The Reality of Latin American Connectivity

12/04/2024

By Peter Wood, Senior Research Analyst at TeleGeography

Originally published in the Telegeography Blog

A few weeks ago, TeleGeography headed back to São Paulo to participate in the Capacity Latin America 2024 conference.

There were few dull moments, with the Latin American wholesale connectivity market full of activity. Among the many discussion points, a few key themes are worth mentioning.

Let’s have a look.

Keeping up With the Connectivity Market

Many cable systems in the region are over 20 years old, approaching the end of their lifespans, and will likely be retired by the end of the decade. This means there’s a need to refresh the cable infrastructure on many routes.

One area of particular focus this year: Central America and the Caribbean.

This is where multiple subsea systems were activated in 2000 (Americas-II, Maya-1, South American Crossing, Pan-American Crossing, Mid-Atlantic Crossing, GlobeNet) and 2001 (ARCOS, South America-1). Each system is different, but in general they are approaching the end of their economic lifetimes.

It can be challenging for carriers to calculate exactly when to officially retire a system and replace it with something new. In Central America and the Caribbean, this is especially difficult.

Demand is relatively low for each individual market, the cost of building and maintaining a new system might exceed anticipated revenue, and permitting can quickly get complicated if a system affects multiple countries.

Extreme Makeover: Submarine Cable Edition

Old cables may be reaching the end of their days, but new infrastructure is on the horizon. And a lot of that infrastructure is headed to Mexico.

Some projects to note are TAM-1 (expected to be ready for service in 2025), TIKAL-AMX3 (2026), and Gold Data-1/Liberty Networks-1 (2026).

Amazon Web Services is also planning a new cloud region in Mexico. Combined with the rapidly growing number of data centers in and near Querétaro and Mexico City, the need for backbone connectivity in Mexico will likely keep rising.

As subsea supply to the Mexican market grows, it will have to compete with very competitively priced terrestrial connectivity in the region.

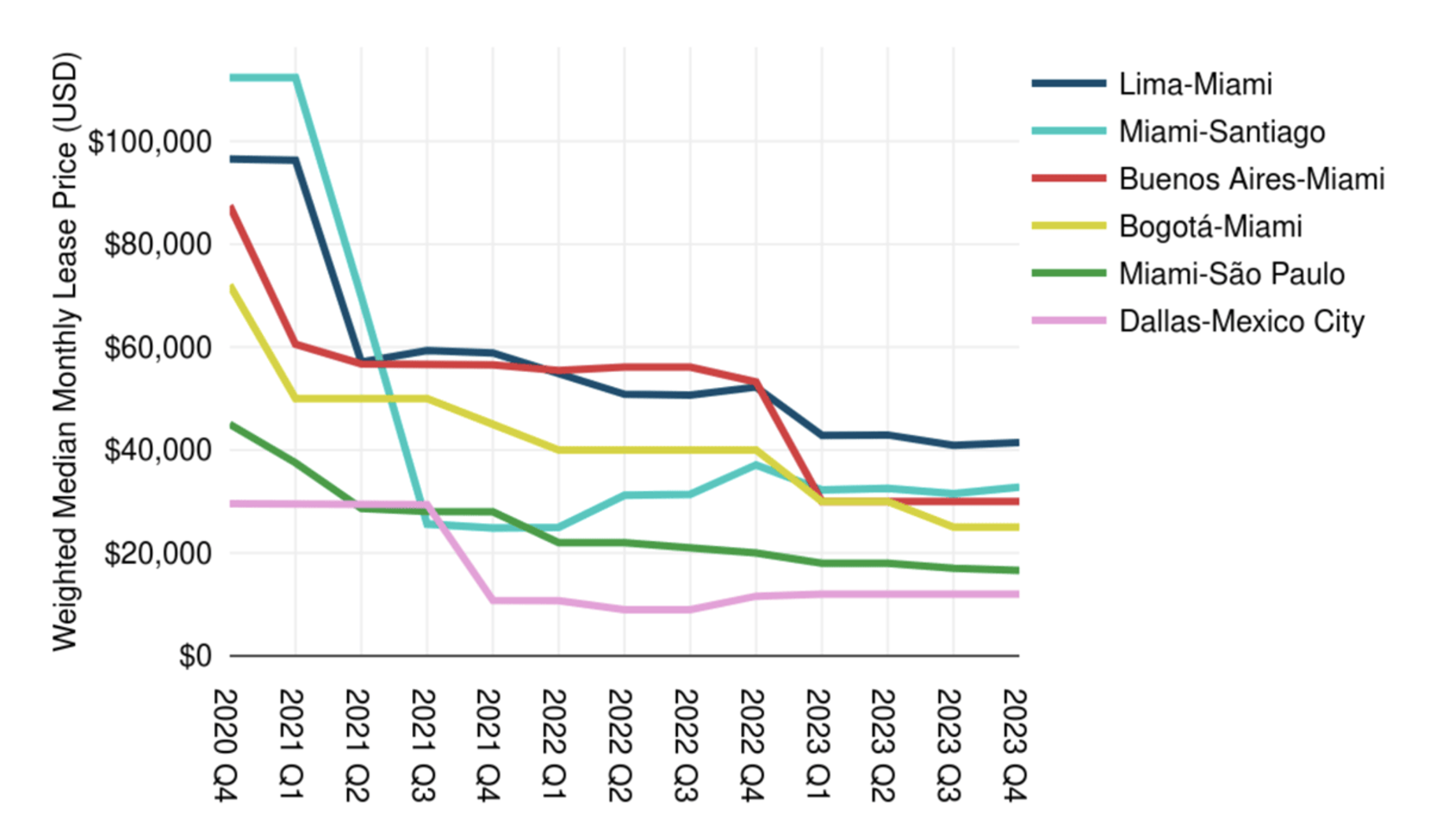

Take the Dallas–Mexico City route as an example. Perhaps the primary route connecting Mexico to the United States, we continually hear it is one of the cheapest in Latin America.

In Q4 2023, the weighted median price for 100 Gbps was $12,000. As supply keeps increasing and the market remains competitive, we expect that price to continue falling.

Source: © 2024 TeleGeography

The Great Brazilian Price Erosion Show

Moving further south, the Brazilian market was also a hot topic at Capacity LATAM. More specifically, attendees were interested in learning about prices for transport and IP transit in Brazil.

The brief summary? Prices have fallen rapidly. And they seem poised to keep doing so. Compounded annually from 2020 to 2023 on Miami–São Paulo, the principal transport route for South America, the weighted median cost of 100 Gbps fell 28% to $16,585.

For IP transit, the situation is similarly impressive. Many providers tell us they offer flat pricing across the country’s key markets of São Paulo, Rio de Janeiro, and Fortaleza. With a Q4 2023 10 GigE weighted median cost of about $0.30 per Mbps, this means that all three cities are among some of the most competitively priced IP transit markets in the world.

For context, the weighted median price for a 10 GigE port in São Paulo in 2018 was six times more expensive than a comparable port in Miami. In Q4 2023, that same port was only 1.6 times more expensive.

As the figure below shows, IP transit is now priced competitively enough in markets like São Paulo to make local transit in Brazil a cheaper option than the traditional purchase of transport to the U.S. plus local IP transit in Miami.

Source: © 2024 TeleGeography

Capacity Latin America may be over for now, but TeleGeography will continue to analyze key trends as the international telecommunications marketplace evolves.

And with upcoming conferences like ITW in National Harbor, Maryland, there will be no shortage of opportunities to discuss new projects and analyze their impact.

The views expressed are those of the author of this blog post and do not necessarily reflect the views of LACNIC.