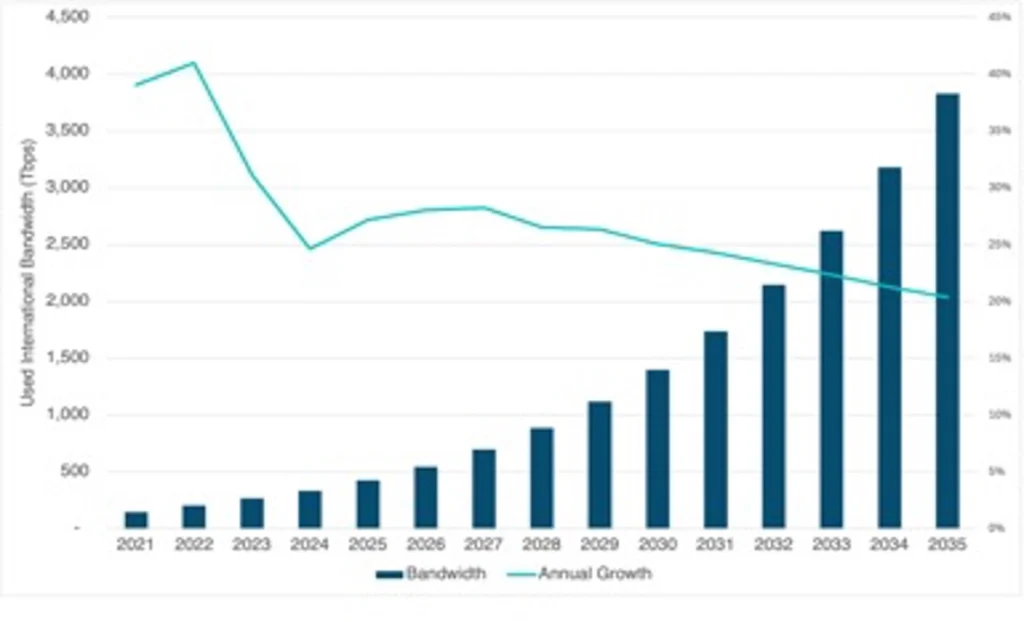

Bandwidth demand continues to grow at slower rates

International bandwidth demand in Latin America continues to rise, although growth rates are decelerating steadily. This broadly mirrors international bandwidth demand trends seen at the global level, where annual growth has fallen below 30% for the second consecutive year in 2025. More localized content in regional hubs, like São Paulo, may have reduced the need for international capacity and thus affected demand growth. We also may be entering a new phase of network buildout in LATAM and, typically, as markets become more mature, we expect growth rates to slow down (as we have seen in Europe, for example). Even as these growth rates have dipped, aggregate demand in Latin America and the Caribbean more than tripled between 2021 and 2025, reaching over 400 Tbps.

Looking ahead we expect growth rates to continue to decline slowly. However, even at a 20% annual growth rate, we project international bandwidth demand could reach over 1.3 Pbps in 2030 and over 3.5 Pbps by 2035. Questions remain about the impact of AI demand on international bandwidth and developments in this area could have a major impact on growth rates (in either direction).

Used International Bandwidth in Latin America (Tbps), 2021-35

(Free access, no subscription required)

Source: TeleGeography Transport Networks and Transport Networks Forecast Research Services

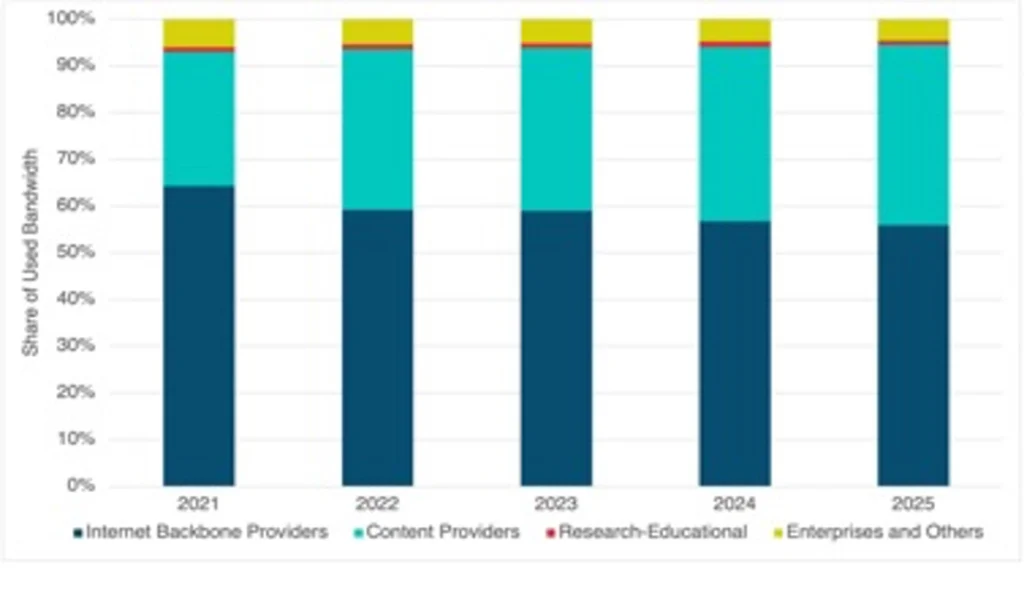

Content providers, the future of demand growth

Content network operators have an increasingly visible presence all around the world, and Latin America is no exception. These companies are expanding their geographic reach and are owners and anchor customers of new cable systems, cloud connectivity, and data centers. Content provider investment has continued in the region, with new infrastructure ensuring they can handle AI training and inferencing.

In 2021, content providers only accounted for 21% of the total used bandwidth for the region, in 2025 this figure was up to almost 40%. Given the large discrepancy between relative growth rates of content providers (41% CAGR between 2021-25) and carriers (26% CAGR between 2021-25), we expect the majority of used bandwidth in the region will come from content providers in the future. TeleGeography’s forecast models indicate that between 2025 and 2035 content providers could have a CAGR of 27%. During this period Internet backbone providers are only expected to reach a 23% CAGR.

Source: TeleGeography Transport Networks and Transport Networks Forecast Research Services

Content providers, the future of demand growth

Content network operators have an increasingly visible presence all around the world, and Latin America is no exception. These companies are expanding their geographic reach and are owners and anchor customers of new cable systems, cloud connectivity, and data centers. Content provider investment has continued in the region, with new infrastructure ensuring they can handle AI training and inferencing.

In 2021, content providers only accounted for 21% of the total used bandwidth for the region, in 2025 this figure was up to almost 40%. Given the large discrepancy between relative growth rates of content providers (41% CAGR between 2021-25) and carriers (26% CAGR between 2021-25), we expect the majority of used bandwidth in the region will come from content providers in the future. TeleGeography’s forecast models indicate that between 2025 and 2035 content providers could have a CAGR of 27%. During this period Internet backbone providers are only expected to reach a 23% CAGR.

Share of Used International Bandwidth by Source for Latin America, 2021-25

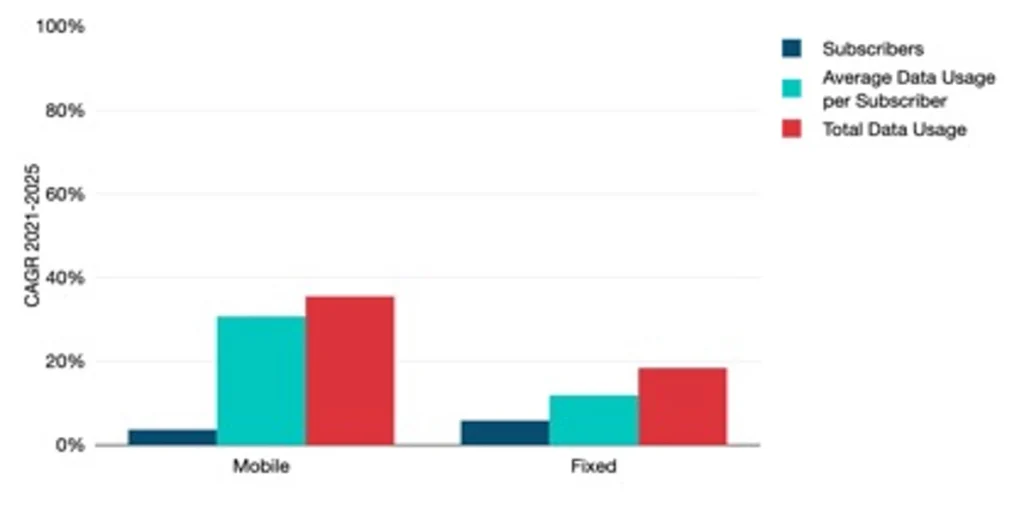

Data usage continues to soar

What is really driving bandwidth demand growth in LATAM? In the graph below you can see the growth in subscribers, average data usage per subscriber, and total data usage for both fixed and mobile devices. The region continues to gain new subscribers at very modest rates for both fixed and mobile devices. Most of the growth is coming from a boost in the average data usage per subscriber. Mobile devices reached a CAGR of over 36% between 2021 and 2025 for average data usage per subscriber, while fixed devices achieved around a 18% CAGR during this time. As we adopt new technologies and increasingly bandwidth-intensive applications, we can expect total data usage to continue to rise even as the growth of new subscribers dries out.

Change in End-User Subscribers and Data Usage in Latin America, 2021-25

Source: TeleGeography IP Networks

New submarine cable projects for LATAM

Following several years of relatively few submarine cable projects in Latin America, the scenario is beginning to shift. Multiple new submarine cable systems are in the planning process, with some cables ready to enter service later this year.

Most of these projects will continue to provide a direct connection to the United States. TAM-1 and Firmina are the first in line. Firmina is now fully active, while both the north and south route of TAM-1 are expected to be ready in 2026. The CSN-1 and TIKAL-AMX3 cables should also be ready this year. All of these new high-capacity cables focus on providing a direct connection to the United States and prepare for the expected growth of demand from content providers. The MANTA cable, another cable connecting to the United States, is expected to be in service in 2028.

New cables are also being planned both within the region and to other regions. Liberty Networks recently announced a new project that will connect El Salvador to Panama. This would be the first submarine cable to connect to El Salvador. Meta’s project Waterworth will provide a direct route from Brazil to both the United States and South Africa. The massive project also has landings in India, Malaysia, and Australia. Finally, Ellalink has announced plans for a branch to French Guiana, which is expected to be in service in 2026. The cable currently provides Brazil with a direct connection to Portugal, Morocco, and Cape Verde.

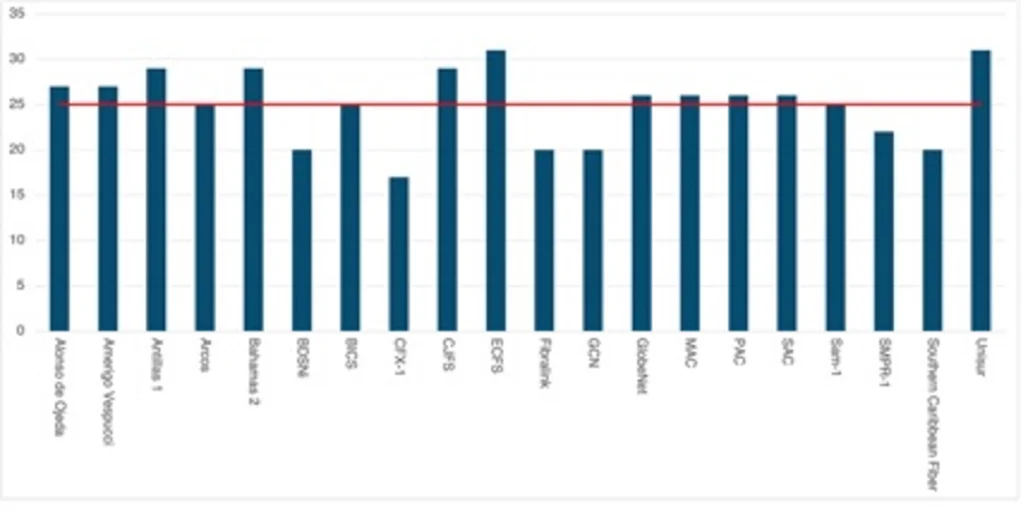

These new cables will help meet the ever-growing bandwidth demand for Latin America while also addressing the need to replace some of the older cable systems in the region. Typically, submarine cables are engineered to have a minimum design life of 25 years. The actual lifespan may differ as it is more closely tied to the cable’s economic life (determined by the cable’s revenues exceeding its costs) and whether the submarine cable is repeatered or not. The 25-year timeline applies to repeatered systems, while shorter unrepeatered systems could function indefinitely. Still, it is important to note the number of cables in Latin America and the Caribbean that are nearing or have recently passed this 25-year threshold (see the figure below). This would suggest that by the end of this decade some of these systems will be retired and replaced.

Submarine Cables Connected to Latin America and the Caribbean with a Ready for Service Date before 2009

Source: TeleGeography’s Transport Networks Research Service

Wavelength prices continue to drop

The transport market in Latin America continues to be dynamic. On key routes from hubs like São Paulo, Bogotá, and Mexico City to the United States, high-capacity sales at low per-unit costs are typical. Yet in areas with less demand, less established infrastructure, or more limited carrier competition, 10 Gbps capacities and lower are still common.

Generally speaking, the same trend holds true across Latin America: prices are declining steadily. Across all routes we track connecting the U.S. and Latin America, the weighted median price for 100 Gbps wavelengths fell an average of 20%, compounded annually, from 2022-2025. The weighted median price for 10 Gbps, in comparison, fell just 12% during that same period. Although 10 Gbps is an important product in many markets, we more often see 100 Gbps as the capacity of choice in Latin America. And in the markets where supply and competition are robust, the cost of 100 Gbps has fallen impressively.

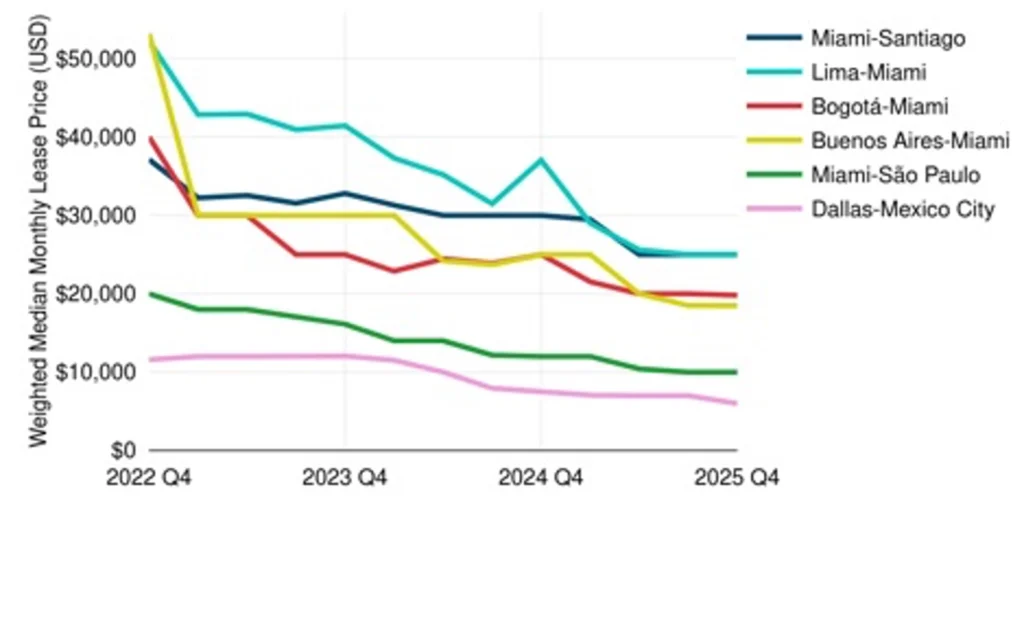

Price erosion remains commonplace throughout Latin America. But the rate of erosion varies by route. The below figure helps us visualize this better by showing recent price decline on key Latin American routes. From 2022-2025, we saw the weighted median price of 100 Gbps on these routes fall an average of 21%, compounded annually.

Weighted Median 100 Gbps Wavelength Prices on Key Latin American Routes

Source: TeleGeography Transport Networks

As you can see above, Miami–São Paulo and Dallas–Mexico City continue to be the most competitively priced routes in the region. These are both very established markets where supply, demand, and competition are abundant. One noteworthy difference between them is that Dallas–Mexico is a shorter terrestrial route, which leads to lower costs (and, in turn, lower prices for buyers) than a subsea route like Miami–São Paulo.

Separately, steep price erosion has brought the Buenos Aires–Miami and Lima–Miami routes in line with others in the region. From 2022-2025, the weighted median price of 100 Gbps on Buenos Aires–Miami fell 30%, compounded annually. For Lima–Miami the price of 100 Gbps fell 22% over the same time period. This comes as both markets have seen increased competition and global carriers offering highly competitive prices.

Bogotá–Miami connectivity is also competitively priced and will likely get even cheaper. The weighted median cost for 100 Gbps on Bogotá–Miami in Q4 2025 was down 21%, compounded annually, from 2022.

New capacity will accelerate price decline

After several years of slow growth, Latin America and the Caribbean are beginning to see a wave of new subsea systems bring additional capacity to the marketplace. This includes recently launched cables like Firmina and others like CSN-1, TAM-1, MANTA, TIKAL/AMX-3, CELIA, and Project Waterworth expected to enter service in the coming one to two years. This increased supply will push 100 Gbps prices downward, especially on routes with ample competition. After that, we expect 400 Gbps sales to become more common on established routes with strong demand in the region.

Beyond more established markets like Miami–São Paulo, we expect prices to continue to fall throughout the region. And in markets where new capacity is expected to come online, higher capacity purchases will become more attractive to customers. For countries like Mexico, that means 400 Gbps sales will become more common. In smaller markets like most Caribbean islands, that will eventually mean 100 Gbps wavelengths are sold more frequently.

The views expressed by the authors of this blog are their own and do not necessarily reflect the views of LACNIC.